A few weeks ago, I bumped into this promising R package, named Bimets (for additional information, see here and here). It has been developed by the research staff of the Bank of Italy.

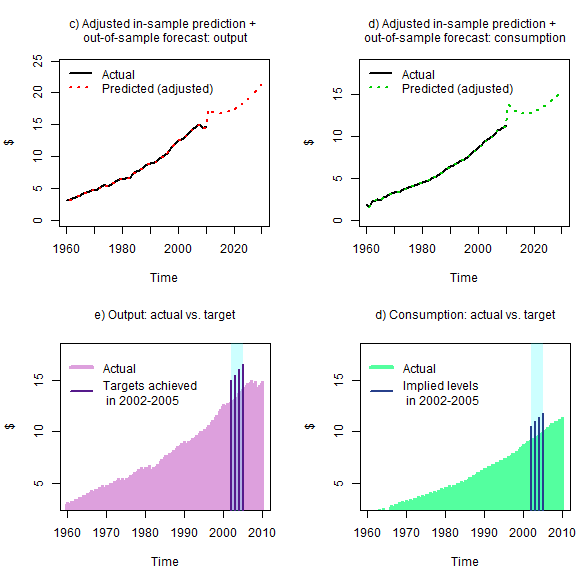

Bimets allows estimating and simulating simultaneous equation models. I have tested it by replicating Model SIM from Godley and Lavoie (2007). I have used mock data inspired to the US time series.

While Model SIM is far too simplified to be used for predictions, this code helps clarify how the Bimets package can be used to estimate empirically SFC model coefficients.

Ah, I was about to forget. Here is the link to the code: bimets_sim. Comments are welcome!